The Complete Guide To Income Protection

Nobody wants to think about being unable to work due to illness or injury. However, it is important to protect your family’s income in the event of not being able to work.

Employer sick pay does not last indefinitely and social welfare payments are a safety net but would probably not pay for all of your bills and expenses. This is where income protection insurance comes in.

Table of Content

What is your most valuable asset?

Common answers for a person’s most valuable asset may include the family home, pensions and/or personal investment portfolios.

While the actual answer might differ from person to person, in many cases, it’s none of the aforementioned suggestions. Oftentimes, the most valuable asset that’s owned by an individual is their ability to earn an income.

For example, take a newly qualified accountant working for one of the Big 4 financial services firms. He/she is likely around 25 years old.

According to Morgan McKinley, newly qualified accountants from the Big 4 are the most in-demand workers within the accountancy and finance space. Such workers command a salary of between €60,000-€70,000 per annum in Dublin.

Over the course of their career, these workers will very likely have salaries in excess of €100,000 per annum for prolonged periods of time.

If we assume that the individual will earn an average salary of €90,000 per annum over 35 years (i.e. to age 60) then he/she will earn €3,150,000 before tax over the course of their working life.

Assuming an effective tax rate of 35%, we’re left with €2,047,500. We then need to account for the time value of money and arrive at the present value of the worker’s future cash flows.

To do this, we need to assume a discount rate. There is much debate as to what’s an appropriate discount rate to use, but for argument’s sake, we’ll assume 3%.

The present value of €2,047,500 over 35 years assuming a discount rate of 3% is €1,257,002. Therefore, we can value the workers ability to earn an income at €1,257,002 – quite a valuable asset indeed.

The value of our respective abilities to earn an income will depend on the income levels that we can command within our respective lines of work, years until retirement, taxation and the discount rate assumed. But clearly, our ability to earn money is incredibly valuable.

If we were to lose our ability to earn money, say, due to an injury or serious illness, both our present and future financial stability could be placed into jeopardy. This is because a loss of household income upon sickness or disability can create what is known as an “income protection gap”.

According to Zurich, income protection gaps are not only damaging to households but also to businesses, governments and the economy as a whole. This is because income protection gaps have the capacity to undermine productivity within the workforce.

This phenomenon (i.e. working while sick because you can’t afford to not work) is known as “presenteeism” and it costs U.S businesses an estimated $150bn per year!

One solution to the problem for all stakeholders is income protection insurance.

Compare income protection insurance quotes from every insurer.

Take our 90-second online assessment and get the best income protection insurance quotes on the market. Our vetted income protection insurance partners are regulated by the Central Bank of Ireland and will outline the various options available to you.

Income Protection

Income Protection Insurance Providers

Deferred Periods

Where an individual suffers a loss of earnings by virtue of not being able to work due to sickness and/or disability, payment under an income protection policy will only take effect in the event that the sickness and/or disability lasts for longer than the “deferred period” which is specified in the policy.

Deferred periods can typically be 13, 26 or 52 weeks in duration.

A shorter deferred period will result in a higher insurance premium given that the benefit becomes payable sooner.

Depending on the policy terms, a deferred period may only have to be fulfilled once where future claims under the income protection policy arise from the same cause of the original loss of earnings (i.e. where the same sickness and/or disability causes recurring periods of loss of income).

Income Protection Payouts

Similar to other insurance policies, certain restrictions may apply to income protection policies and payouts arising from such.

For example, where an individual engages in deliberate non-disclosure of material facts about their medical history and current health status. In their income protection underwriting guide Aviva highlight a number of medical conditions that would influence the underwriting process and would therefore need to be disclosed (this is not an exhaustive list):

Furthermore, Aviva notes certain medical conditions which may make an application for income protection unacceptable. These include, but are not limited to:

However, where payouts are made under an income protection policy (i.e. where it is proven that the individual is unable to carry out the essential duties of their job or based on another metric), they will continue until the earlier of the following events:

Individuals who return to work either part-time or in a lower income role than they were in before the original claim may receive what’s known as a “rehab benefit”.

In such a circumstance, the life insurance company would continue to pay part of the income benefit payable under the policy in addition to the individual’s new income.

The rationale behind such a benefit is to encourage a partial return to work where medically possible.

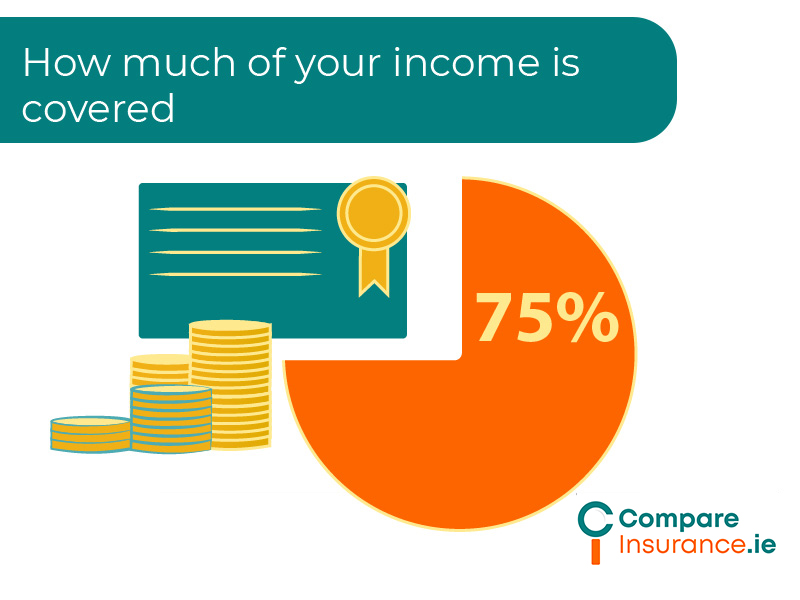

In terms of how much cash is payable under an income protection policy, the maximum you can receive as per the CCPC is equal to 75% of pre-disability earnings less your State illness benefit entitlement and any sick pay you receive.

As an example, say your salary was equal to €60,000 and you insured that income up to the maximum permissible limit of 75% (i.e. €45,000).

If you received the maximum State illness benefit of €12,064, then the maximum benefit payable under the policy would be €32,936 per annum or €2,745 per month.

The reason why a cap of 75% is applied is because the life insurance companies will always want to make sure that there’s a financial incentive for the policyholder to return to work. The life insurance companies will typically restrict the maximum benefit that’s payable in any given year under the policy.

For example, in the case of Aviva, the maximum annual benefit that’s payable is €250,000 (per year) before indexation.

The maximum benefit calculation can differ between company directors, self-employed persons, employees and homemakers/carers. Note that certain life insurance companies will permit employer contributions to the employee’s approved pension scheme to be covered.

Make no mistake about it, payouts from life insurance companies under income protection policies can and do happen.

In 2022, Aviva paid out a record €48M to customers with income protection insurance. The primary causation for claims was psychological issues & mental health.

According to their website, 56% of claims came from women to which the average annual payment was €34,500. The remaining 44% came from men to which the average annual payment was €51,000.

Similarly, in 2022, Zurich handled claims from 360 claimants and are paying over €9M annually in claims.

How Compare Insurance Works

We compare all insurance options so you can be sure you’re always getting the best deal.

1. Select Your Product

Simply select the insurance product you need a quote for e.g. life, home or health insurance.

2. Online Quote Form

Fill out one of our simple online assessments with your insurance details.

3. Free Quote Consultation

A qualified financial advisor will call you back for your free insurance quotation.

Income Protection Premiums

Many individuals with income protection cover have obtained that cover through employer group schemes. In accordance with Revenue guidance, PAYE taxpayers can get tax relief on income protection premiums paid by way of deduction at source by their employer.

Relief from income tax is afforded at the individual’s marginal rate up to an annual limit of 10% of total income. Note that USC and PRSI are still applicable. Your employer may also contribute money towards the payment of premiums and, where this occurs, only USC is payable on the contributions. Where the combined contributions of both the employee and employer exceed 10% of the employee’s income, income tax and PRSI will apply to the excess.

In return for the payment of a premium, an income protection policy will provide a fixed level of cover for the term of the policy. Similar to other policies, the policyholder may opt to include an “indexation option” whereby the level of cover is increased (irrespective of health status) in return for a higher premium.

How much premium you pay is largely dependent on the nature of your occupation.

For example, premiums will typically be “banded” whereby low risk occupations pay the lowest premiums and high risk occupations pay the highest premiums.

The occupational classifications are as follows:

Certain occupations may be too risky to insure, including occupations where the individual works:

Examples of denied occupations may include:

Where the life insurance company feels that the risk is higher than what was accounted for by the actuaries in their regular premium pricing, an extra premium up to a specified percentage may be charged. This is referred to as “premium loading”.

Where the risk is too great for premium loading, but is not so great that it can’t be covered, the life insurance company may offer coverage but with an exclusion that prevents a payout in the event of sickness and/or disability due to the identified risk.

Factors To Consider: Income Protection

Income Protection Ireland – Get your free quote today!

We compare the market so you don’t have to. Take our online assessment to find the best income protection quote for you today.

Speak with Ireland’s leading insurance comparison website today and start saving on your insurance.